Hello!

It has been a while! For those that have worked with me over the past 10 years or so you would be familiar with my content you will see below. I write about once a month specifically to the brave realtors in the trenches helping our home buyers find the perfect home but certainly can be relatable to our home buyer clients. The content consists of a recap in the financial markets to offer insight on what happened regarding interest rates as well as real estate related to our local market in Clark County. I hope you find it useful. This is also available in audio in the link below. Enjoy!

What's Goin On (Audio Version)

Financial Markets- Stocks

This section will be particularly long today so I can provide a baseline of information and there is a lot to cover to untangle misconceptions about mortgage rates. Future write ups will not be as dry and lengthy, but this may be one you may want to archive.

The latest rapid sell off in the stock market started around the 3rd week of April and can be attributed to the war in Eastern Europe and the increased likelihood that the US Economy is headed for a recession in light of the Fed’s commitment to tame inflation. More in-depth discussion on this below.

Financial Markets- Bonds (Mortgage Rates)

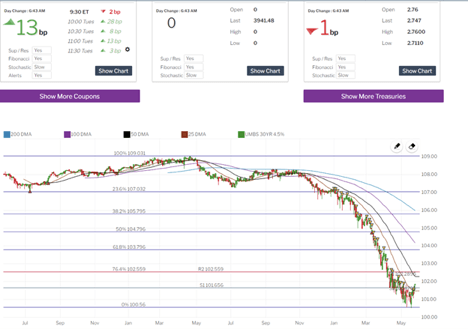

As for bonds, well it has been a steady downward spiral for the past year with most of the damage inflicted in the past 4 months. The bond market is where mortgage-backed securities are traded. As a whole when the bond market is selling off, the price of mortgage-backed securities are going down and the yield, or mortgage rate to the customer is going up. This graph below illustrates a 2 year look at a 30-year mortgage backed security and you can see the price was around “109” in May of 2021. In just one year the price of this bond dropped to around “101”. This is a drop of “800 basis points”. Generally speaking, 100 basis points = .25%, so 800 basis points equates to an increase in mortgage rates of around 2%.

So what the heck happened to mortgage rates??

Two primary reasons for this drastic increase in mortgage rates:

1)Around January 1 of 2022 is when the analysts and economists concluded that inflation was not just temporary, that it was here to stay and it was very real. Monthly Inflation reports such as the “CPI” (Consumer Price Index) indicated inflation running over 8%. For perspective, inflation rates didn’t surpass 4% for nearly 40 years.

https://www.macrotrends.net/countries/USA/united-states/inflation-rate-cpi

So, for investors investing in the bond market, if their rate of return is 3%, and inflation is running at 8%, they are losing 5% a year by staying invested in that investment vehicle. Simply put the price of bonds will keep going down until the yield of the bond, or rate of return from that bond, hovers around the rate of inflation. Remember that the rate of return to a bond investor is the interest rate to a home loan customer.

2)The Fed was a big buyer of mortgage backed securities throughout covid in order to artificially keep mortgage rates low and they decided to significantly reduce buying mortgage backed securities and allowed the open market to set the price at the beginning of the year. This was a double whammy, we had a sell off in mortgage backed securities because of inflation and the biggest customer, the fed, stopped buying them as well. The end result, supply massively outweighed demand, the price of the mortgage backed securities dropped (from 109 to 101) and the yield, aka, the customer’s mortgage rate went up 2%.

But the Fed is about to raise the rates again, so mortgage rates are going up right???!!!

The biggest misconception regarding the Fed Reserve’s maneuvers and how it affects mortgage rates is that the Fed can’t directly raise or lower mortgage rates. When we hear about the Fed raising rates, the rate they are raising is NOT a mortgage rate, remember mortgage rates hinge off the buying and selling of mortgage-backed securities in the bond market. The rate the Fed controls and is the “Federal Funds Rate”. This is a rate in which banks borrow overnight. As this rate increases it becomes more expensive for banks to borrow, they in turn raise rates issued to the consumer for credit cards, home equity line of credits and other various bank loans. This then has an indirect impact on the bond market and in particular mortgage backed securities but doesn’t translate into an increase in mortgage rates just because the “Fed raised THE rates”.

Why is the Fed Raising rates?

The Fed is raising rates for one simple reason. Get inflation under control! For the better part of 40 years the rate of inflation ran around 3% or less. For the past few months inflation according to the CPI has been running over 8%. We can all relate to how much this sucks! Gas prices, lumber, meat, fruit, etc, everything costs more today and it sucks for the consumer because our paychecks haven’t gone up. The Fed has come to the realization that inflation wasn’t just about covid and supply chain issues. If you ask me, It was from a combination of increase in minimum wages, the government handouts, reduction in oil production making fuel more expensive AND yes, supply chain issues. The Fed now has to apply the emergency brake on the US economy, not just tap the brakes, but slam on the brakes and create legit skid marks in the road, smokin tires and all. By raising the Fed Funds Rate (the rate in which banks borrow money overnight), banks then turning around and raising rates on credit cards and other various bank loans issued to consumers it eventually curbs the consumer’s appetite to spend. The Consumer consumes less and businesses are able to manufacture at a pace to meet the demand of the consumer which finally leads to price stabilization in all goods. The collateral damage is that we most likely end up in a recession, with higher unemployment and less wage growth.

Pop quiz: What will happen to mortgage rates if inflation settles back down to 2% (extra credit if you can explain why?)

Answer: Mortgage rates drift back down because mortgage-backed securities and bonds in general become an attractive investment again with inflation running at 2%.

Conclusion: The Fed Raising Rates should in the long run result in lower mortgage rates, but it will take some time.

Stay tuned for next month on why buyers are having to pay points right now when locking in the rate.

Southern Nevada Real Estate

April home sales for Clark County followed the trend that has taken shape for 2022, less transactions and higher prices. April median priced home of $475,000 shattered the prior high broken in March by $15,000 and up over 26% from April 2021. 3,001 transactions took place, down over 8% from March 2022 and down nearly 15% from April 2021. This is the necessary pain the local real estate market needs to help supply and demand get back to equilibrium. It won’t be fun getting there but certainly it will be a more healthy real estate market for our home buyers if we can get to 3-4 months’ supply.

A special salute to our men and women that serve and have served on this Memorial Day. Enjoy the weekend, I will be on call to help with financing if you need me.

Cheers!