This week’s blog will focus on a less talked about obstacle for home buyers, the cost of interest rates and why it is difficult to find “par” or “0 points”. Before we start, I want to highlight a few of the many benefits to partnering with The Maltese Mortgage Group powered by Cardinal Financial:

- Current time from contract to final approval is 23.35 days (under 20 when stripping out new construction).

- Under 8% of applications end up getting suspended and under 2% end up not closing.

- 2022 YTD ranked in the top 25 in loan volume for Clark County, NV licensed loan officers

- All 5-star reviews on Google!

By partnering with me, you and your entire client database can be enrolled in List Reports and Home Bot. Rate Plug will help you provide customized financing packages for your listings so you can advertise payment. (Below are links if you are unfamiliar with these tools)

https://welcome.listreports.com/

Look for me in in Rate Plug so you can offer customized loan estimates through the MLS!

https://www.rateplug.com/member/default.asp

Financial Markets- Stocks

Stocks continue to slide with the inflation report released at a higher than expected 9.1%. Analysts are also cringing at the prospects of a poor upcoming 2nd quarter earnings season. The Dow is down nearly 350 points this week. “Stagflation” is being floated with some anaylists predicting it to be a real possiblity. (Staglation is when the economy stops growing and still experiences inflation, not where inflation goes to a dance by him/herself….budum pshhhht. I’ll be here all week, try the veal)

Financial Markets- Bonds (Mortgage Rates)

After reaching a peak of nearly 3.5%, the 10 year US Treasury showed signs of improvement touching down to around 2.9%, but since has elevated back up above 3%. This puts the typical 30 year fixed rate mortgage in the high 5’s but what is creating additoinal head winds for borrowers is the cost of the rates.

Because mortgage rates have gone up so significantly its difficult for lenders to offer at rate at “0 pts” otherwise known as “par”. This is because investors that purchase mortgage-backed securities don’t expect mortgages funding today to have the typical lifespan as mortgages that funded withing the past few years. The average lifespan of a 30 year mortgage is 5.5 years and investors in mortgage-backed securities, essentially the market in which all mortgage companies sell their loans in, would typically pay a certain premium based on that life expectancy. Since the life expectancy of the mortgages today is much shorter, these investrors are not paying the same premium and as a result mortgage companies have no choice but to collect the shortgage from the borrower upfront in the form of “points”. Its not uncommon for a borrower to pay anywhere from 1 to 3 points on primary residences and even more on investment properties.

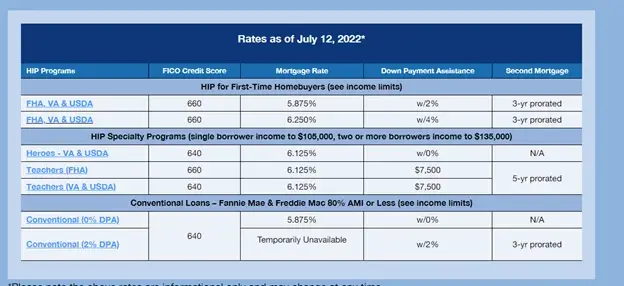

This also explains why there are very few down payment assistance options. Down payment assistance often comes in the form of a higher rate. The investor pays a higher premium at the higher rate and that higher premium is passed on to the borrower under the label of “down payment assistance”. But because of the explanations mentioned above, there is really no market for even higher rates. Below is Home is Possible’s most recent down payment assistance rate sheet. The menu of products has been cut by 50% from this time a year ago.

Southern Nevada Real Estate

June sales for Clark County provided a strong signal that the market is in the process of building much needed inventory. The median price finally leveled. For the first time in 2 years, down a smidge to $480,000. This is still up over 20% from June of 2021. Just over 3,400 properties exchanged hands for the month which is down nearly 25% from June 2021. With the number of transactions decreasing and listings increasing the market in Southern Nevada went from just two to three weeks of housing supply to 2 months’ supply seemingly overnight. Adding to the pain for the mortgage industry, cash purchases made up 30% of the sales for June, undoubtedly due to the higher interest rates.

Remember that traditionally real estate appreciation of 5% a year is considered healthy. Las Vegas has averaged over 15% the past 5 years and over 20% the past 3 years, so a correction is nothing to panic about.