Conventional loan limit for 2024 has increased to $766,550

- A buyer can put as little as 3% down on a sales price up to $790,000 (if they are a first-time home buyer)

- A buyer can put as little as 5% down on a sales price up to $807,000.

- A buyer can put as little as 10% down on a sales price up to $1,407,000 (by coupling a conventional loan with a 2nd mortgage line of credit)

Cardinals’ in-house DPA: Cardinal National Home Buyer Assistance program is a great substitute for buyers that don’t qualify for Home Is Possible, below is a side-by-side comparison of where the program can help:

| Requirements | CNHA | HIP |

| Min FICO | 600 | 640 |

| Max Income | Unlimited | $103,195 |

| Must be 1st time HB | No | Yes |

| Max sales price | Unlimited | $504,081 |

| Max DTI | 57% | 45% |

| DPA amount | 3.5% of sales price | Up to 4% of loan amount |

*Only compatible with FHA loans. Message me for details!

Financial Markets- Stocks

Stocks are capping off one of the better months in recent times, up nearly 8% for the month. The Dow as I write this is knocking on the door of 36,000 and approaching its all-time high. A personal consumption price index report, which is a measure of inflation came in at 3.5% from the same month last year, which was 2 tenths lower than last months’ report. That report coupled with the Fed indicating they are done raising rates along with consensus that the US economy seems to be structurally strong all contributed to November’s strong stock market performance.

https://www.cnbc.com/2023/11/29/stock-market-today-live-updates.html

Financial Markets- Bonds (Mortgage Rates)

FIIIINALLLY, a bond market rally with some legs that began shortly after my last newsletter (end of October) has begun. The average 30 year fixed rate mortgage peaked at roughly 8% at the end of October and has now drifted down to just over 7% as of the end of November. Below we can see that the 10 year US Treasury touched around 5% at the end of October and today hovers at around 4.3%. The US Treasury and mortgage rates don’t move perfectly together. If you remember in prior newsletters I mentioned that the typical spread between the 10 year US Treasury and the average 30 year fixed rate mortgage was typically 2% or less, and if that traditional spread existed today it would place the 30 year fixed rate mortgage closer to 6.25% or less…Nonetheless, they are tethered fairly close together and is a good instrument to use to see what’s happening real time with mortgage rates.

https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed

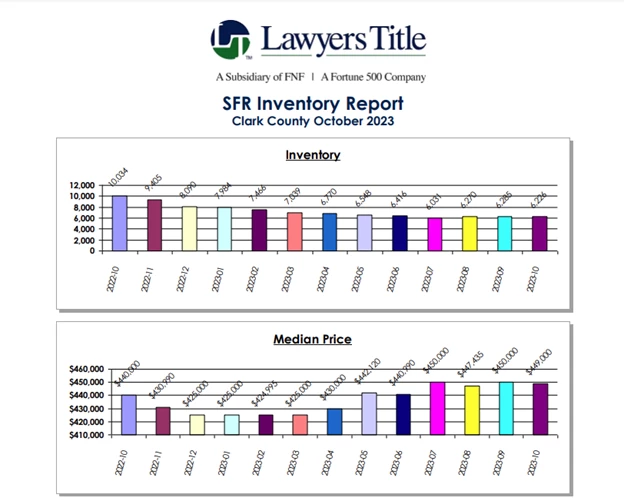

Southern Nevada Real Estate

October sales for Southern Nevada continue to show strength in value but weakness in volume. Around 2,740 total transactions took place for the month of October, 345 condos, 313 townhomes and 2,082 single family residences. The 2,740 is roughly 40% off the pace of 2019 (what I call the last normal year). Consistent with a typical October we have started to see an increase in inventory. Roughly 6,200 single family homes on the market translate into roughly 3.5 months supply and should help keep prices in check for the time being. Although with the 2024 spring season around the corner and rates beginning to fall this price pause button may not stay paused very long, but for the moment the median priced SFR has stayed stagnant at around $450,000 for the 4th straight month.

Message me for access to the following cutting edge realtor tools, Homebot, List Reports and Rate Plug at no cost to you!

List Reports brief description video:

https://listreports.wistia.com/medias/u3n951yoyu

Homebot brief description video:

Rate Plug brief description video: