Click here for Audio

Financial Markets- Stocks

The month of September was a bloody month for stocks in general, The Dow Jones is on the brink of dipping below 29,000, representing a nearly 13% decline for the month. All the focus is on inflation. The latest sell off is actually in light of a more positive than expected unemployment report. The thought process among investors is that if the job market is strong, the Fed will continue to raise rates which is bad for corporate profits and growth. Ordinarily the stock market would react favorably to a better than expected job report. Welcome to Bizzaro World.

Financial Markets- Bonds (Mortgage Rates)

Often the bond market reaps the benefits of stock sell off, and mortgage rates would typically improve in light of our sagging 401k accounts. Not this month. Bonds also got crushed. The bond market is where mortgage backed securities are traded and what mortgage rates hinge off of. Remember that our home buyer’s interest rate is the rate of return of investors investing in mortgage-backed securities. In the past month the price of the 5% UMBS (Uniform Mortgage Backed Security) went from a price of 101 to as low as 97, representing a nearly 1% increase in mortgage rates. In many instances you can find 30 year fixed mortgage at around 7% now.

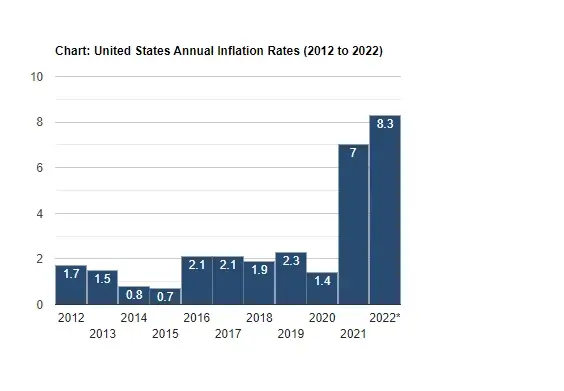

The silver lining is that inflation numbers will start to look much better very soon. Inflation guages the month we are in vs the same month last year. The November inflation report, representing inflation for October, is really where the alarms started sounding. Core inflation rose from 4% (September 2020 vs September 2021) to 4.6% (October 2020 vs October 2021). The Fed likes to see this number at around 2%. In hind stie the Fed should have initiated some sort of tightening policy then if not sooner.

Below is a link to an inflation calculator and every inflation report for as far back as you would like to go.

https://www.usinflationcalculator.com/

Southern Nevada Real Estate

Does it feel like securing home loans are getting more difficult or that underwriting in general is getting more strict? If it does you aren’t alone. It is said that the “scratch and dent market” (Where lenders sell loans if for some reason Fannie Mae, Fredde Mac or Ginne Mae reject the purchase of a loan) is any where from 60 to 70 cents on the dollar. This means that if a mortgage company closes a loan they end up not selling because they didn’t collect the proper documentation, instead of making a 3-5% profit of the loan amount ($400,000 x 5% = $20,000), they could lose as much as $160,000 reselling it on the scratch and dent market. Talk about pressure!

Product News- New Releases

· Fix and Flip Financing up to $1,000,000

· Conventional loans up to $715,000 as of right now!

· Construction-to-perm loans up to $3,000,000

· Cash out refinance for Foreign Nationals

· 2/1 Buydown

Call me for free access to the following Realtor Tools!