Important Product Updates!

3-2-1 buy downs now for FHA, Conventional and VA. This means the buyer could have a start rate of 3.5% in year 1, 4.5% in year 2, 5.5% in year 3 and finally 6.5% in year 4. On a $400,000 loan amount this would cost around $17,000 in cost or 4.3%. Remember that the unused savings will go back to the buyer if they sell or refinance the home within the first 4 years.

Conventional loan limits up to $726,000.

This means a buyer can put in theory as little as 3% down up to $748,000. (In most cases it would require 5% down though up to $764,000 sales price). This also means by doing a 1st and 2nd mortgage the buyer can finance up to 90% of the purchase price up to $1,350,000 sales price.

FHA loan limits as of January 1, 2023 will increase to $472,030

VA Loan Limits up to $2,000,000

Cardinal has rolled out its construction to perm portfolio for Conventional FHA and VA. The buyer can also have a manufactured home installed on the land and roll it all into one loan.

Last, keep in mind we can help buyers and borrowers in all 50 states

Financial Markets- Stocks

Stocks are up marginally since last months’ commentary. The market rallied with a friendlier than expected Consumer Price Index Report, in which inflation was considered to be subsiding. The next CPI report will come out on December 13th which also coincides with the next Fed meeting and there is sure to be some market volatility or “chop” as they say. The other focal point for the markets was the jobs report released this past Friday which came in stronger than expected. Despite the Fed Rate hikes all year the US still added over 250,000 jobs. Unemployment rate ticked up to 3.7% from 3.5%. The most impactful component of the report however was hourly earnings, up .6% for the month, which annualized would be an increase of 7% a year. Wage increases indicated in this latest jobs report only adds pressure to the Fed’s inflation concerns and increases the likelihood of more rate hikes. This is why stocks sold off over the past few days. Bizarre right? A good jobs report ordinarily would instigate a stock market rally.

https://www.cnbc.com/2022/12/02/jobs-report-november-2022.html

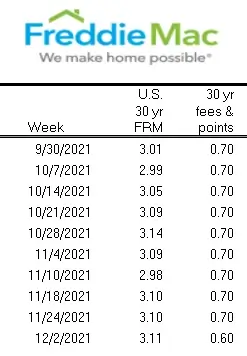

Financial Markets- Bonds (Mortgage Rates)

For the same reasons stocks sold off, bonds sold off and mortgage rates lost some of its gains from last month. The jobs report and most particularly the average hourly rate increase of .6% was much higher than expected. The average 30 year fixed mortgage for the past week was around 6.5%. Remember that this is with the buyer paying nearly 1 pt on average. The same week last year the average 30 year fixed was just over 3% and the average cost in terms of points was around 6.

https://www.freddiemac.com/pmms

Southern Nevada Real Estate

November home sales for Clark County followed a similar trend as the last several months. The median priced home dropped another $10,000, landing at just over $430,990. This marks a decrease of around 11% from the peak of the market where the median priced home was just over $480,000 in May of this past year. Transactionally, the market is down over 50% from the same month last year. Just 1,521 single family resale homes exchanged hands this past month. With 7,342 homes on the market this translates into nearly a 5 month supply of homes. This seems a bit misleading because in a normal market this would look more like a 2 month supply.

So that’s the million dollar question isn’t it? When will the market return to “normal” from a transactions stand point? Transactionally we really didn’t experience a slow down until around the spring of 2022. Because I am a numbers guy I will say that the lack of appetite from a buyer’s perspective is payment based and not price based. If the median priced home was $460,000 and the rate was say around 3.75% around that time and the appetite for buyers was “healthy” then what will it take to get back to that point from a monthly payment perspective? If rates hold at 6.5% than the median priced home would need to drift down to $350,000 for the buyer to have a similar payment as what they would have had in March of 2022. At the rate of roughly 2% home value depreciation per month we would reach this point by September of 2023. However, if rates drop 1.5% then the median priced home would have to drop to around $410,000. At the current rate of home value deprecation we could reach this point by March of 2023. So that’s my guess, somewhere between March and September of next year is when we can expect to see a more “normal” market from a transactional stand point. Call it May. And with that said, if we don’t see a noticeable amount of inventory hit the market we could once again be talking about housing shortages, paying over appraised value and accelerated home value AAAAA-preciation

Message me for free access to the following Realtor Tools!