Click here to watch on YouTube

Product Highlight of the month - “DSCR”

We’ve heard this phrase quite a bit over the past several years so I wanted to take a deep dive into how the product works and realistically what you as the realtor can expect. First, DSCR is an acronym for “debt service coverage ratio”. This program is designed for investment properties. Most of the guidelines don’t care about your debt-to-income ratio, and don’t care to see your pay stubs, tax returns, etc. It simply compares the mortgage payment vs the proposed rent the property will generate. If the mortgage payment is $3,000 per month, and the proposed rent is $3,000 per month, this would be considered a “1:1” ratio. If the mortgage payment is $3600 per month and the estimated rent value comes in at $3,000 per month, this would be considered a .8: 1 ratio, and would result in a higher interest rate, further widening the gap between the mortgage payment and the proposed rent, and possibly pushing it so far out of range that the loan loses its approval.

While in theory, these programs will lend up to 80% of the value of the home, the reality is, that if the investor plans on putting only 20% down the proposed rents most likely won’t come close to covering the mortgage payment, at least not in Las Vegas. The “ratio” would be well under 1 with just 20% down. To make matters worse no one will know what the proposed rent will be until the appraisal comes in…well after the buyer is under contract.

The buyer should be prepared for a minimum of 40% down in order to avoid a stressful and turbulent transaction. If they are “pre-approved” for a DSCR with a loan to value of say 75% just know that the approval could fall apart after the appraisal comes back.

With the fearmongering of the DSCR program out of the way, If the buyer is prepared for 40-50% down, the upside is it will be an easy process with very little paperwork required and the interest rates are often in the 7’s, and competitive to a conventional investment property loan. In short, this is a great program with 40% + down.

Financial Markets- Stocks

The S&P 500 is off to a roaring start to 2024, just 52 days into the year and the index is up nearly 400 pts or up over 8%. Better than expected unemployment numbers along with Mega chip manufacturing company Nvidia beating expectations were the primary catalysts for the market gains.

https://www.cnbc.com/quotes/.SPX

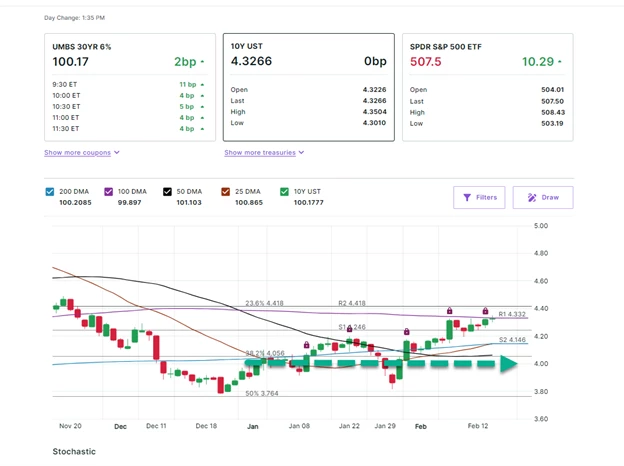

Financial Markets- Bonds (Mortgage Rates)

The bond market, and mortgage-backed securities in particular did not fare as well as the S&P to start the year. To start 2024, the 10-year US Treasury had drifted below 4%, but as we turned the page to February, hotter than expected employment reports and hotter than expected inflation reports triggered a noticeable sell-off in the bond market and particularly, mortgage-backed securities. The average 30-year fixed went from roughly 6.6% to up over 7.1% in a matter of 2 short weeks. The reports also created doubt that the Federal Reserve would start to lower the Federal Funds Rate, also known as the “prime rate” in March, and it's looking like summer at best that the Fed would start to take any easing action.

The current spread between the 10-year US Treasury and the average 30-year fixed is around 2.7%. The spread was as high as 3.3% at one point last year and has started to drift closer to a historical spread of around 2%.

Southern Nevada Real Estate

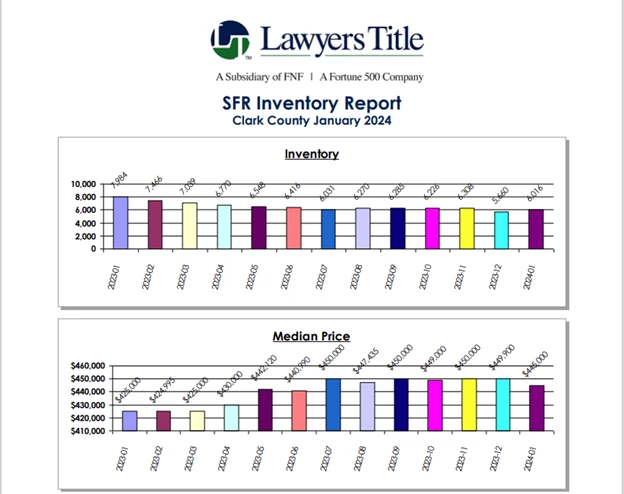

The first month of 2024 showed noticeable signs of improvement in terms of the number of transactions that took place in Clark County. 1,717 Single-family residences, 338 condos, and 302 townhomes exchanged hands in January 2024, for a total of 2,357 transactions, up nearly 350 transactions from January 2023, or a 17% increase year over year. The median-priced home in Clark County inched down $5,000 from $449,000 to $445,000 from December 2023, but up $25,000 from the same month last year, for a nearly 6% gain year over year. Inventory for SFRs increased from roughly 5,500 available homes to just over 6,000 homes, translating into a 3.5-month supply of single-family residence homes. Roughly 33% of the homes were paid with cash, which is on the high side historically speaking.

Message me for access to the following cutting edge realtor tools, Homebot, List Reports and Rate Plug at no cost to you!

List Reports brief description video:

https://listreports.wistia.com/medias/u3n951yoyu

Homebot brief description video:

Rate Plug brief description video:

https://www.rateplug.com/Agents.asp?UName=LVR