Audio Version

Hello and welcome back! There is a treasure trove of important data released over the past several days and I want to get right to it but before I do I need to clean up parts of my commentary from last month regarding 2-1 buy downs. If you missed it, a 2-1 buy down is where rates start out at 2% below current rates in year 1, move 1% higher in year 2, and finally caps out at the current rate in year 3 and stays there the remaining 28 years. So, as an example, if a 30-year fixed was 7% today, in year one it would be 5%, year 2 would be 6%, year 3 would be 7%. On a $400,000 mortgage this would save somewhere around $500 a month or $6,000 in year 1, $250 a month or $3,000 in year 2. The cost to participate is the savings over 2 years, or in this case, $8,000. What I missed in the last commentary is that if the buyer refinances at any time before the 2 years, the buyer gets the refund of any unused savings. So, let’s say the buyer refinances in 12 months, and there is $3,000 left in unused savings, the buyer will have that $3,000 applied towards the payoff.

The 2-1 buy down is the most effective way to use seller contributions if the buyer is on a budget and looking to keep mortgage payments lower.

Financial Markets- Stocks

The stock markets are enjoying a sorely needed rally today, with the dow up over 1,000 points for the day, partially because the uncertainty of the election results is starting to come into focus, and primarily because the inflation report released this morning. This marks the Dow up nearly 10% in the past month. Next week we may start to get the courage up to look at our 401ks and IRA’s.

Financial Markets- Bonds (Mortgage Rates)

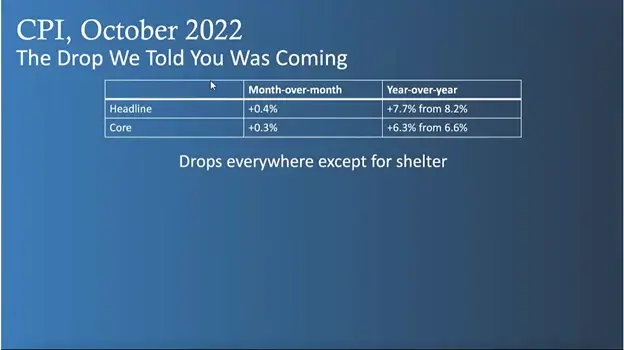

Now, for the really good stuff. The turkey if you will, of Thanksgiving dinner, the Sour Patch Kids of your Halloween bag of candy. Today’s inflation report is exactly what mortgage bonds have been waiting for. For the first time in nearly 2 years, inflation is subsiding. The highlights are are the Core Inflation (which strips out Gas/energy) is up just .3% month over month. This means that over the course of a year inflation would be around 3.6%. Year over year the CPI is still up 7.7%, but the market expected 8%.

With inflation trending in the right direction it makes mortgage-backed securities an attractive investment. As an example, if the rate of return is say 6% and inflation is running at 3.5%, then it becomes a great place to invest for a virtually risk free investment. The graph below shows how ugly it had gotten over the past year. This mortgage backed security was trading at a price of nearly 112 at this time last year. By around 3 weeks ago, where we hope mortgage rates will have peaked, the price of this bond bottomed out to a price of nearly 97. This represents a 1500 basis point difference. Generally speaking, 100 bps is equivalent to .25% in interest rate on a 30 year fixed mortgage. We are talking a nearly 4% increase in interest rates in just 1 year. Today, we gained back, at least for a day anyway, about 1/10th of that move in rates. The prognosis is that rates will continue to drop and settle somewhere between high 4’s and mid 5’s over the course of the next 6-12 months.

Southern Nevada Real Estate

The look back at the last year of interest rates helps understand the latest October home sales report for Southern Nevada. 1,724 single family residences exchanged hands last month, down from over 3,000 transactions in October of 2021. With nearly 8,000 homes listed for sale without offers this represents a 4.5 month supply of homes. The median priced home dropped to $440,000, which is down nearly 10% from the peak price of $482,000 in May. It will most likely take a combination of further price decreases and continued improvement to interest rates before we will see normal levels of purchase transactions. The saying goes “It’s darkest before dawn” well, with the release of today’s inflation report, we may have our darkest moments in the rear view mirror. Now is a great time for buyers to get prequalified. Not suggesting it’s the best time to buy but certainly a great time to start preparing to buy. If prices dropped another 10% and rates drop another 2%, from an affordability stand point we would be back to 2021 levels where sales were among its highest levels in Southern Nevada real estate history.

Product News- New Releases

· Fix and Flip Financing up to $1,000,000

· Conventional loans up to $700,000 as of right now!

· Construction-to-perm loans up to $3,000,000

· Cash out refinance for Foreign Nationals

· 2-1 Buy Downs for Conventional and FHA

· Investment property purchases with no income verification

Message me for free access to the following Realtor Tools!